Tax Cooperation in an Unjust World

New book just published: Tax Cooperation in an Unjust World

This Wednesday: Last Tax Policy Colloquium of the year, with Kyle Willmott

Kyle Willmott presents in the last tax policy colloquium of 2021.

Tomorrow: Tax Policy Colloquium with Donatella Alessandrini

Donatella Alessandrini presents in this week’s tax policy colloquium.

Tomorrow: Tax Policy Colloquium with Irma Mosquera

Irma Mosquera presents in this week’s tax policy colloquium.

Tomorrow: Tax Policy Colloquium with Suranjali Tandon

Suranjali Tandon presents in this week’s tax policy colloquium

This Wednesday: Tax Policy Colloquium with Wei Cui

Wei Cui presents in this week’s tax policy colloquium

Tax Policy Colloquium today at McGill: Clair Quentin

Clair Quentin presents in this week’s tax policy colloquium

McGill Fall 2021 Tax Policy Colloquium

The fall Tax Policy Colloquium will start on Oct 7 and all are invited to attend …

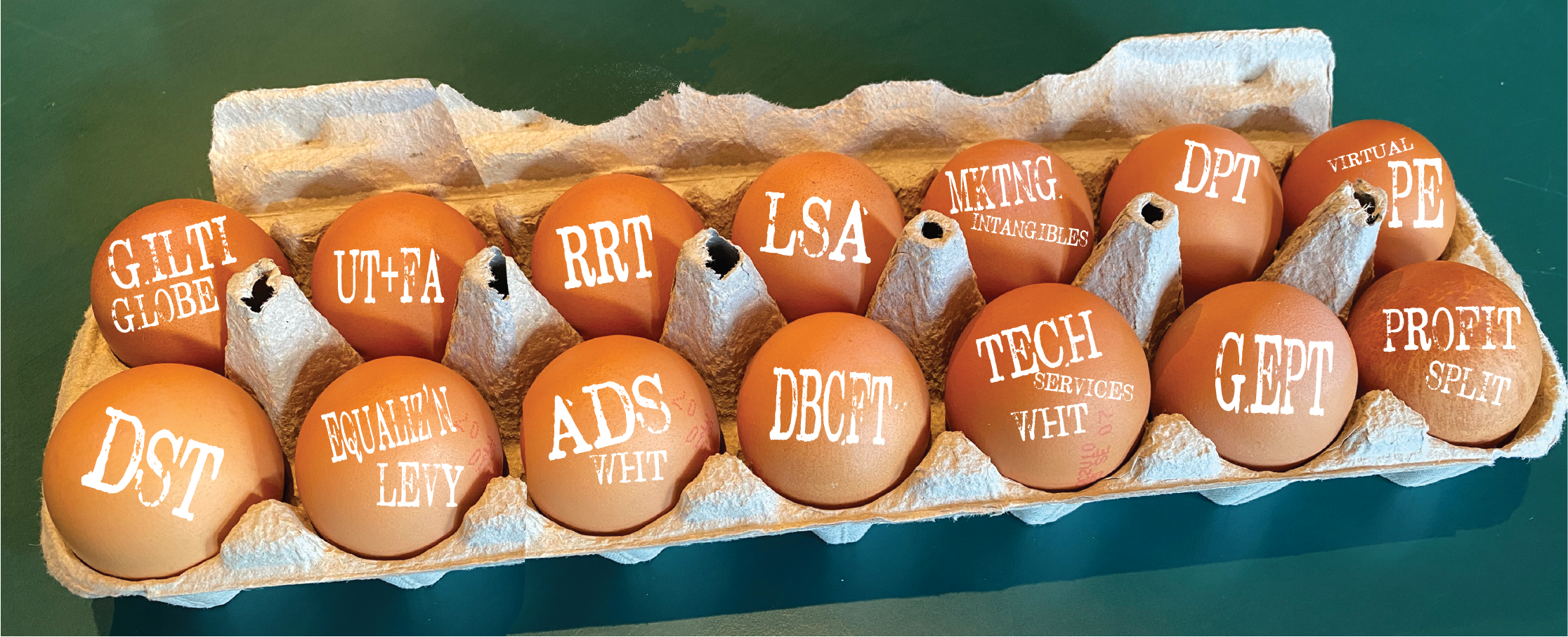

The final BEPS plan has clicked into place: here it is in pictures

There is still much to be worked out but this is an exciting if also confounding moment for international tax.

The Rise of Cooperative Surplus Taxation

Confused about what’s happening in international tax?

McGill Fall 2020 Tax Policy Colloquium

Lineup for the Fall 2020 McGill Tax Policy Colloquium: All talks will take place via zoom and all are welcome.

Accurately counting value in the international tax system

Here is my presentation for today’s IU/Leeds Summer Tax Workshop Series…

Finance Ministers’ Reply to Mnuchin

And here is the reply from the four finance ministers to Secretary Mnuchin…